At Pennypack Ecological Restoration Trust, PA, USA.

At Pennypack Ecological Restoration Trust, PA, USA.

I had just finished making a video for one of my classes, when I looked out the window, saw the sky, and rushed to the best vantage point the house offers for the sunset to shoot this photo.

The 2020 Bank of Sweden Prize in Economic Sciences in Honor of Alfred Nobel was awarded today jointly to Paul Milgrom and Robert Wilson of Stanford University for their work in Auction theory. Here is the popular information document on the Nobel Prize website, complete with some really great graphics: https://www.nobelprize.org/prizes/economic-sciences/2020/popular-information/

Hearty congratulations to the winners! More from me on this blog a little later. I know a bit about auction theory and have taught parts of the theory — now I will prepare a lecture on this award to be delivered on October 23d. Details to follow.

Shot with Fujifilm X-T2, edited in Affinity Photo

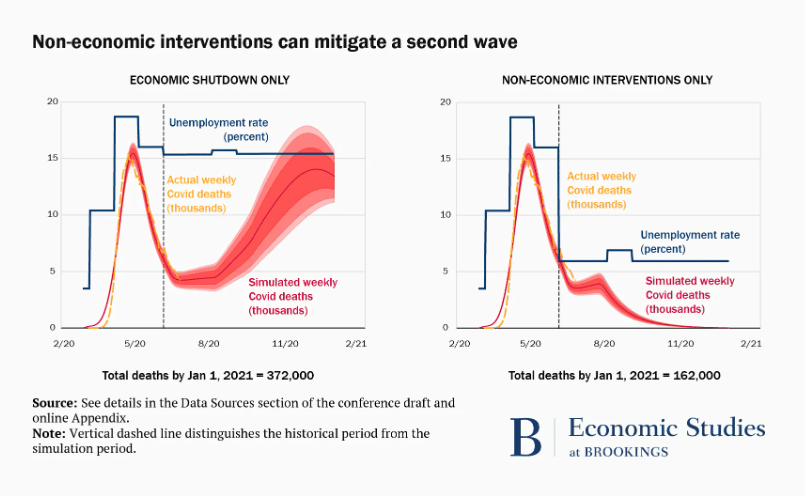

The Brookings Papers on Economic Activity mini-conference on COVID-19 happened today as a webinar. I am reading several of the paper drafts that were discussed (but did not have the chance to tune in to the webinar). I may write more here about these papers, but for now I want to emphasize this graph from the paper by Baqaee et al., Policies for a Second Wave:

The graph is self-contained, so I don’t feel the need to explain it more.

I may indeed post again, in more detail, about this and other papers presented in this conference.

The paper “Simulating COVID-19 in a University Environment“, written by Philip T. Gressman and Jennifer R. Peck appeared in ArXiv on June 5, 2020. It contains a stochastic agent-based model that simulates the likely progress of COVID-19 disease transmission in a fictional U.S. University with 20,000 students and 2,500 faculty members that opens for a semester of 100 days in a world with certain (unknown) members of the general population infected with the disease. It also includes an analytical model that supports the main conclusions drawn from the simulations. It complements the paper “The small world network of college classes: Implications for epidemic spread on a university campus” by K. A. Weeden and B. Cornwell.

How to open a University campus relatively safely and conduct instruction with minimal numbers of infection and the maximal possible effectiveness of instruction is keeping University and College administrators up at night, not to mention faculty members like myself, who dread the possibility of being forced to teach in a classroom at a risk to their health they deem too high. Papers like the Gressman and Peck paper are valuable contributions to administrators’ decision-making and I hope they are taken seriously by them.

The main conclusions of the paper can be summarized simply. I do so now and I discuss the assumptions of the paper at the end of this blog post. The two outcomes the simulations focus on to evaluate the effectiveness of various infection control measures are (1) the total number of infections and (2) peak quarantine population.

Disclaimer: I read with reasonable care the main body of the paper and glanced at the part of the appendix where the results of robustness testing are reported. I did not read the analytical model presented at the end of the appendix, Section 5.3.

Main conclusions of the simulations:

I found the paper convincing and its conclusions credible. I do want to emphasize some limitations of the analysis of the paper stemming from its assumptions. These are mostly made clear by the authors but do tend to push in the direction of making the conclusions overoptimistic. I offer these critical comments as a caution for readers, especially should they be University administrators, and not in order to diminish the contribution of the authors; obviously, all analyses have their limitations.

I could offer more minor nitpicking comments on the assumptions of the analysis, but I am stopping here, after having listed my main thoughts about the limitations of the paper. I view it as a very good and interesting paper and I look forward to additional simulations along the lines of those it offers that expand the reach of the model with assumptions amended along the lines I outlined in my critique.

The paper “How Did COVID-19 and Stabilization Policies Affect Spending and Employment? A New Real-Time Economic Tracker Based on Private Sector Data”, by Raj Chetty, John N. Friedman, Nathaniel Hendren, Michael Steiner, and the Opportunity Insights Team, was released on June 17, 2020. The authors have created a new freely accessible online tracker that allows you to see the evolution over time of many data series that give an idea of how the US economy and society are recovering from the COVID-19 pandemic. Both the paper and the tracker are highly recommended. Visit the tracker here: https://tracktherecovery.org/. To give you a flavor of what data the tracker contains and the visualizations it makes available, here are two screenshots from the home page. There is a wealth of data in the tracker and the visitor can create and almost endless variety of graphical representations of selected data sets.

I thought I’d post some more flower photos. I make several of those with my iPhone when on my daily constitutional. Click or tap on a photo to see it full size.

To finish tonight’s spate of photo posts, here is one from our walk yesterday. This, and the other three I just published, were all made on an iPhone 11 XR and edited in Snapseed.